On the first of July, we all took off our masks and it seems that our lives are slowly returning to normal after the coronavirus crisis.

How this will affect the mortgage and real estate market in the coming months , we will discuss in today’s article.

So let’s go through all the changes that have taken place over the last few months and how they will manifest themselves in the coming period.

More affordable mortgages for all

The CNB (Czech National Bank) recently abolished the DTI and DSTI parameters and moved the recommended LTV limit to 90%. We have already discussed what these parameters mean in an earlier Article

In short, the CNB has transferred the responsibility of examining income back to the banks. And just as banks have relaxed the limits on 90% mortgages, that is, mortgages where you only need 10% cash to buy your home.

It even allowed banks to take out 100% mortgages in very small numbers (1 in every 20 mortgages).

However, the reality is that, with a few exceptions, banks strictly adhere to the original recommendations. In this respect, the development of mortgages is considerably stunted.

However, if the economic situation develops favourably, we can expect mortgages to become significantly more affordable again.

Reduction of interest rates

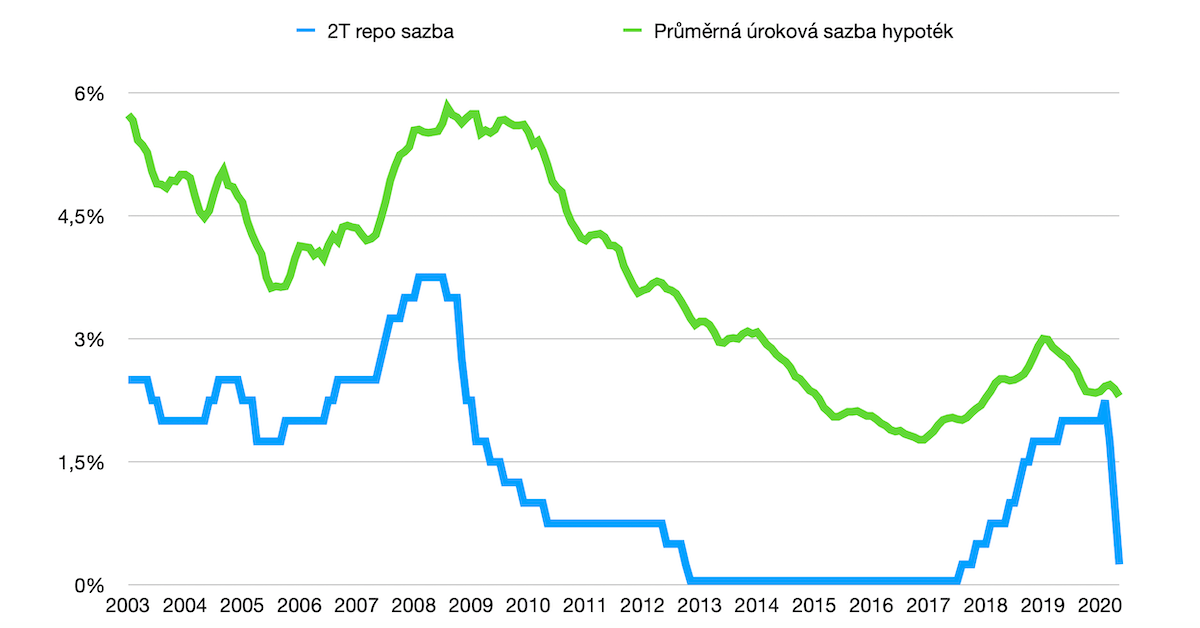

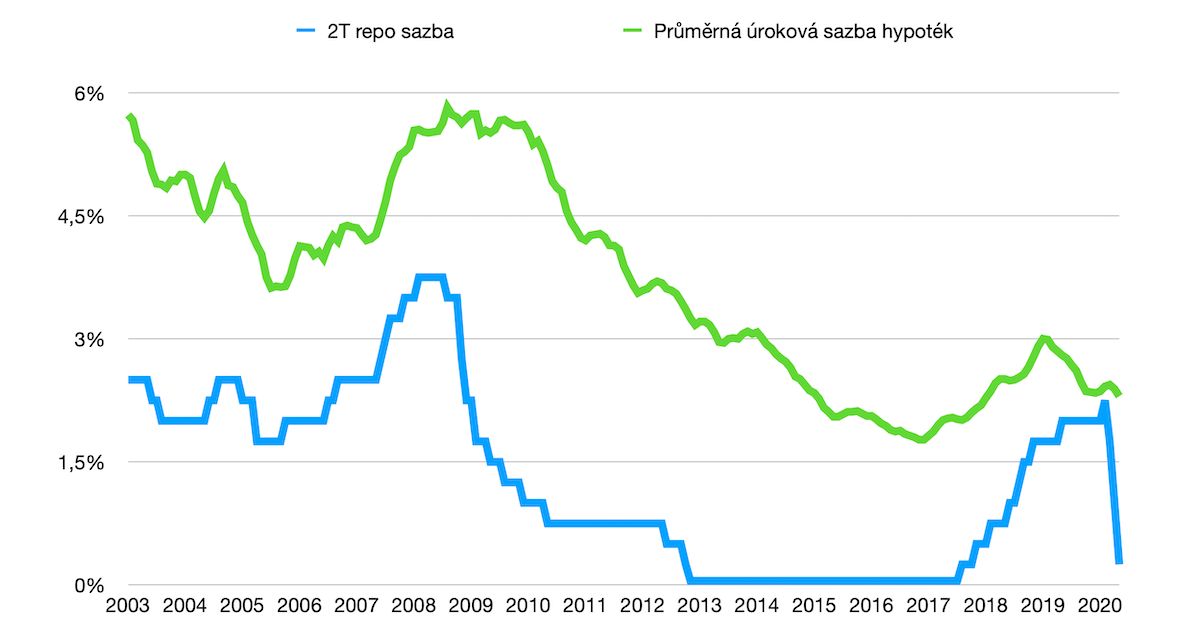

It is no secret that the CNB has also cut the 2T repo rate 3 times since March 2020. For our purposes, let’s call it the “baserate”. Its current value is 0.25%, the lowest level in the last 3 years and very close to the 0.05% level from 2012 to 2017.

The base rate can be loosely translated as the approximate rate at which banks buy. To this must be added the bank’s costs, the risk premium and, of course, the margin or profit of the bank as such.

Below you can see how this base rate has evolved from 2003 to today, along with the average mortgage rate. Note the evolution of mortgages at the end.

We can therefore logically conclude from the chart that mortgages could be arranged at 1.5% p.a. in the coming months.

However, everything will depend on which of the following scenarios occurs.