In today’s article, you will find out in which cases it is worth taking out employers’ liability insurance. We will tell you what is covered and what is not, and how much it will cost you.

What is “bullshit insurance”?

The first thing to note is that the crap insurance policy you have with your home insurance does not cover damage caused by your employer. They are two different products. One is called

Liability insurance in ordinary civil life

and the other

Employee liability insurance for damage caused by the employer

.

So today we will talk about the latter.

By law, the employer may claim compensation from the employee in an amount not exceeding 4.5 times his gross monthly wage. So if you earn 20k. CZK net, which is approx. CZK gross, your employer cannot ask you to pay more than CZK 117,000. And this number should be exactly the same as the sum insured you have set in your insurance policy.

What the policy covers:

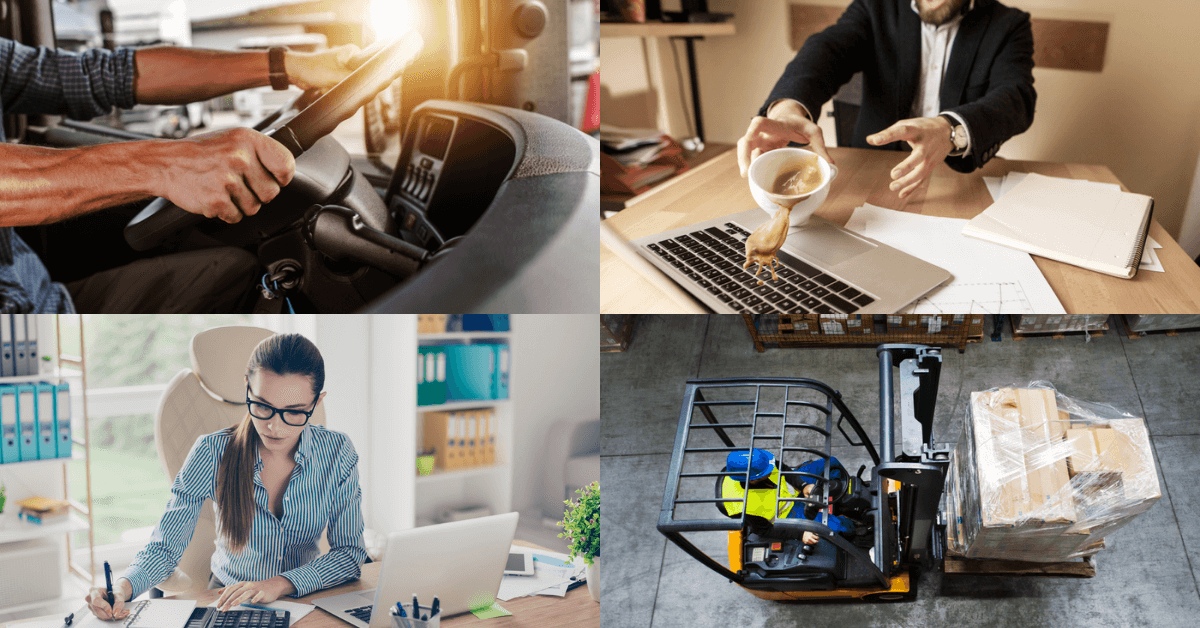

Let’s talk about a few examples from practice:

- You are a warehouseman and you are a lizard going into a shelf with goods.

- You drive a company car and hit a mirror or damage the car in an at-fault accident.

- You have a business laptop or phone and it’s fallen on the floor or spilled coffee on it.

- You’re an accountant, and your mistake was the Social Security Department charging you a fine or penalty.

- You do it manually and you just break something.

What the policy does not cover:

- You are an accountant and you are short of money in the cash register.

- Damage caused as a result of exercising the right of defective performance (claim). Making a mess.

- Damage resulting from alcohol consumption.

- Intentional damage.

Work on agreement (FTE, FTE)

If you are working under a Contract of Employment or a Contract for the Performance of Work, you will have a more limited choice, but you will also find an insurance company that also covers this employment relationship. You can even work for one employer on an HPP and another on a DPP and be covered for both under the same policy.

What to watch out for?

The most common mistake made by clients and, unfortunately, by insurers, is not reading the part of the policy conditions where exclusions are listed. An exclusion is a case where the insurance company fails to pay. It’s usually one short paragraph and after reading it, you get a clear picture. Whenever I arrange this policy for a client, I select the insurance company that will best suit his profession with regard to this very paragraph.

The next thing is setting the deductible. You will always share in some part of the damage. The most common deductible is 10%, with a minimum of CZK 1,000. It doesn’t cost as much as a lower deductible and it doesn’t hurt as much in the event of a claim.

Last but not least, we need to look at the territorial validity. If you are an international truck driver, you will probably find the insurance policy valid only in the Czech Republic useless.

Price

The price depends on which of the following categories you fall into and whether the policy also covers damage to a company car.

- I work in an office and I don’t drive a company car. The price will range from approximately CZK 1,000 to 1,500 per year.

- I only drive a company car occasionally. The price will be around CZK 2,000 – 2,500 per year.

- I drive working machines (e.g.: a lizard) or I am a professional driver. The price will be around 2 500 – 4 000 CZK per year

Conclusion

A crap insurance policy for work is definitely a good thing. However, you need to choose the right one and have the right sum insured and deductible.

If you’re not quite sure about yours, I’d be happy to help.